Deep Dive #3: Uranium Pricing 101

Uranium is the quirkiest commodity market in the world and it is critical that investors understand the basics of price reporting, the types of contracts industry participants utilize and who reports them. In this Deep Dive, we review:

Industry Basics

The Spot Market

Converter Locations & Prices

How Important Is the Spot Market?

The Long-Term Contract Market

Cameco Contracting Talking Points

State of the Contract Market Today

Final Thoughts

Industry Basics

Let us cover the industry basics when it comes to price reporting. There are two industry consultants who are the official price reporters:

Ux Consulting, LLC (UxC)

Tradetech (TT)

Both consulting firms have a long and tenured history in the nuclear fuel industry. Both produce research, cover current market dynamics and report (to the best of their ability) spot and term-contracting volumes along with prices for uranium, conversion and enrichment. It is important for investors realize that there are no exchanges where physical uranium is traded, both for spot and term contracts, so the entire industry is over-the-counter (OTC). While there is a Chicago Mercantile Exchange (CME) futures contract, it has never really gotten off the ground so investors can safely ignore it as it simply is not relevant.

As a result, it is up to market participants (utilities, traders, miners, converters, enrichers, and hedge funds), to report transactions to UxC and/or TT if they wish. Some entities have policies in place to report transactions while others do not. Sometimes, an entity might want a price reporter to know about a transaction at a certain price point while at other times, they wish to transact as quietly as possible. This leads to a lot of the opacity in the industry.

These consultants play an important role as some contracts can be tied to what these firms report. As a simple example, an off-take (to a utility or trading firm) from a producer might be linked to an “official month-end” price or a monthly average of the price (spot MAP). They also do their best to report spot and term volumes in uranium, conversion and enrichment which gives the market a better understanding of current dynamics. We believe the market is better off for having their presence as without them, this industry would be significantly more opaque than it already is.

The Spot Market

The nuclear fuel trade is dominated by long-term contracts as this is where utilities procure 80-90% of their reactor consumption needs. However, the spot market provides a daily snapshot of what is happening. While it remains an important price indicator, it is a small portion of where total transactions occur.

Most commodity investors associate a “spot market” with today’s market. What can be bought or sold today? But, in uranium, the spot market works a bit differently. UxC defines the “Ux U3O8 Price®” (spot) as: “Conditions for delivery timeframe (less than or equal to 3 months), quantity (equal to or more than 100,000-lbs U3O8), and origin considerations” (Ux Price Indictor Definitions, www.uxc.com) Simply put, a spot trade includes a delivery (book transfer at a converter) within three months of today. Origin pertains to the country the material was produced. With the current sanctions in place from Western countries, most of the West is trading any global material ex-Russia. With rising prices in recent years, the market does trade volumes that are not 100K-lbs as the nominal value has increased (100k @ $30/lb = $3M vs. 100K @ $75/lb = $7.5M). It does see 50K-lb lots from time to time but it can be any amount as it is an over-the-counter (OTC) market. As long as two parties agree, the volume can be 20K-lbs, 50K-lbs, 100K-lbs or more.

The “spot price” is usually the most competitive offer available for U3O8 of which UxC is aware, taking into consideration information on bid and transaction prices as well as the timing of bids, offers and transactions with a daily cut-off time of 2:30 PM EST. The Ux U3O8 Price is published daily (excluding certain US holidays).

UxC currently uses two participating brokers, Evolution Markets and Numerco Limited, which collects the best spot bids and offers for prompt delivery (within three months). From this broker data, UxC calculates the UxC Broker Average Bid and the UxC Broker Average Offer.

UxC also uses the “Ux U3O8 Monthly Average Price” (spot MAP) which represents the average of all Monday Ux U3O8 Price for the month. As a side note, month-end in uranium occurs on the last Monday of every month, which might not link up with the actual month end.

Uranium Markets (UM), is another uranium brokerage company that provides daily bids and asks on behalf of their clients using their “Broker Price Indicator.” While separate from the Ux U3O8 and TT spot prices, they provide another “look” at the market based on what their clients are doing. UM provides a morning update with bid/asks at each converter location for specified months along with an end of day email showing their best bid and best ask any all converter locations.

Converter Locations and Prices

The other key piece of information is the U3O8 location pricing. There are three western conversion facilities where U3O8 is stored for commercial storage and trading:

Cameco’s Port Hope Conversion Plant in Port Hope, Ontario, Canada (CMC)

Converdyn’s Metropolis Conversion Plant in Metropolis, Illinois, USA (CVD)

Orano’s Phillipe Coste Conversion Plant in Tricastin, France (ORO)

The spot UxC CMC, CVD, and ORO prices reflect UxC’s determination of prices for U3O8 delivery at the specified delivery location taking into consideration bids, offers and market activity using the same delivery time period, quantity, and origin considerations (www.uxc.com)

These location prices can differ based on market conditions. Eg, at certain times, demand or supply could be significantly higher at one or two converter locations. When this happens, a “location differential” can appear. Using a basic example, if CVD is trading at a $1.00/lb premium over CMC and ORO, there is a $1.00/lb location premium at CVD > CMC/ORO. The CMC, CVD, and ORO are simply converter locations. If a trade is happening at CMC, it does not necessarily mean it is actually Cameco purchasing material (although it could be). It just means a market participant is buying material at the CMC location.

Recently, when President Trump began calling for a new tariff regime, CVD traded at a premium to CMC/ORO. This makes sense as any material already in the United States could not be subject to a tariff whereas material at CMC/ORO could potentially be charged a tariff upon entering the United States. Recently, the location premium at CVD reached ~$2.00/lb over CVD/ORO but has since subsided as the world gets more comfortable with the White House’s tariff policies.

While slightly outside the purview of this piece, holders of U3O8 at one location can “swap” material at another. This tends to become more prevalent when location differentials exist as the holder of material can earn a fee based on the location differential.

Using the recent example above, when CVD was trading ~$2.00/lb premium over CMC/ORO, if an entity held 100K-lbs at CVD and another market participant wanted or needed material at CVD but does not want to physically move it there (it costs money to transport, insure, etc.), they can seek a location swap, where the swap seeker will pay $2.00/lb to the holder of material at CVD and each party will swap U3O8 at each location. The owner of the CVD material will then own U3O8 from another converter, in this case either CVD or ORO and collect $200,000 for doing so and vice versa.

When location differentials exist, UxC blends or averages the prices together to form the “Ux U3O8 Price”, usually with a tilt toward where the bulk of the volume is occurring, as best as they can tell.

It is important to note that unlike other commodities, uranium spot prices can move without an actual trade occurring. If an offer is in the market, but there is no willing buyer, the seller could move the offer down impacting the spot price for a day without a transaction occurring. The reverse can also be true, with an offer being moved up without a transaction. Obviously, this nuance is important, particularly during times of illiquidity as bid/asks can shift around, changing the spot price without any actual transaction occurring. To complicate matters, price reporters do not report daily volumes as they might not even know what traded or how much.

Tradetech uses a similar system to UxC stating: “Similar to TradeTech’s Weekly Uranium Spot Price Indicator and monthly NUEXCO Exchange Value, the Daily Uranium Spot Price Indicator reflects the company’s judgment of the price at which spot and near-term transactions for significant quantities of natural uranium concentrates could be concluded as of the close of business each day.” (“Uranium Prices”, www.uranium.info)

How Important is the Spot Market?

At times, we see investors debate the importance of the spot market given that utilities only source a small portion of their actual fuel needs from it.

At Golden Rock, the spot market is best described as a simple daily snapshot of where active buyers and sellers are trying to transact. It is an important market as it is the only daily reported price but there are a variety of reasons why a buyer or seller would utilize spot and it might not be for purely fundamental reasons. Said differently, we see equity investors constantly complaining about why an entity is selling but we can assure you they they have very different goals than a say, a fundamental equity investor with a long-term view.

As a result, spot prices can easily stray from a deemed fundamental level, both on the upside and downside. From time to time, it can be very illiquid too, so selling a simple 100K-lbs could easily move the market $0.50/lb, $1.00/lb or even $2.00/lb under the right conditions. As a result, investors have been known to fiercely debate the relevance and importance of spot prices.

Traditionally, spot has been used as a “surplus disposal market.” Said differently, producers of U3O8 create the best value for themselves by contracting directly with a utility. Even better, they sign a contract and then produce into that contract. However, not all producers do this. As a result, some sell produced material in the spot market earning the phrase, surplus disposal market.

Generally speaking, when U3O8 enters the spot market (from mine production, inventory sale, etc.), it will be traded or churned over and over again until the material is removed. It is usually removed in the form of a utility directly purchasing it and placing it in their inventory, a carry-trade occurring where a trader can purchase pounds in spot and hold them (carried) until delivery to the utility, or a producer purchases U3O8 to deliver into a utility contract. It is important to realize this structure and how it works. A single 100K-lb lot of U3O8 might trade hands three, five or ten times before it is removed as described above. As a result, spot volumes give an indication of how many pounds might have been traded, but we do not know how many of the same pounds are traded over and over again.

Back to spot dynamics, we feel it is important to understand where bids/asks are available and what the dynamics are in the market at any given time. We recently wrote that we expect to see the delta between spot and long-term prices collapse as utilities try to take advantage of cheaper prices in spot by purchasing material directly or using carry trades. We have begun to see this play out as prices have jumped from ~$63/lb to ~$71-$73/lb this week. See the full write up at the link below:

As a result, we have been quite bullish spot market dynamics since late February/early March as offers began to dry up signaling to us, that whomever needed to sell material has done so. Further, with the significant premium of long-term prices over spot, we felt it was a matter of time until fundamental buyers used it as an opportunity to pluck pounds from the spot market. And it appears that this has been playing out.

We cannot stress how important situational awareness is for this market. There are times where spot plays a more important role than usual and other times where it is rather insignificant. This is a function of how utilities have been procuring, their activity levels and the types of ways they attempt to procure. As a result, we do not feel the spot market always represents one thing, at all times. Like any other market, dynamics shift and the importance of spot or lack thereof shifts.

The Long-Term Contract Market

The long-term contract market is where utilities procure about 80-90% of their reactor needs. For deliveries under long-term contracts, there are two main pricing mechanisms:

Fixed or Specified Pricing

Market-Related Pricing

Fixed pricing is either: a fixed price, a series of fixed prices, or a base price plus an adjustment for inflation to the date of delivery otherwise known as a “base-escalated” contract. The adjustment mechanism in base-escalated contracts is either a combination of published indexes (from UxC or TT) or a fixed annual percentage rate (eg, an inflation rate.)

Fixed or base-escalated contracts is the most predictable form of pricing and is attractive to both buyers and sellers in terms of managing cash flow and budgets. This is very straight-forward as both the seller and utility will know, almost exactly, what they will be paying at time of delivery as every portion of the contract is agreed to in advance.

The only element of uncertainty is if the adjustment mechanism uses a market rate of some kind, like the US Consumer Price or the US Gross Domestic Product price inflators. The adjustment rate can also be defined at a fixed rate lending predictably to both sides of the contract.

The Ux Long-Term U3O8 Price includes conditions for escalation (from the current quarter), delivery timeframe of 36 months or longer from today and quantity flexibility considerations. Lastly, Ux LT U3O8 price is generated by using the lowest base-escalated offer in the market. Tradetech uses similar language for their LT U3O8 price as well. A market-related contract and its floors and ceilings are not included to form the long-term price that is reported.

Market-related contracts are based on the spot price at or near the time of delivery. In most cases, the price is the spot price minus a small discount (or sometimes, plus a small premium).

This type of contract means both the buyer and seller are not sure what the price will actually be at the time of delivery, but gives the parties an opportunity to gain value based on their market views. As a result, buyers usually want some assurances in case prices soar and sellers want to same in case prices drop precipitously. In these cases, if a utility asks for a “price ceiling,” the supplier and buyer will need to agree on maximize price or ceiling. Likewise, a supplier may ask for a “price floor” to protect their downside and both parties will need to agree to a minimum price or floor.

These floor and ceilings prices can operate much in the same way as a base-escalated contract where floors and ceiling can escalate as time passes to protect the real value of the contract.

Contracts can also be a combination of fixed/base-escalated and market-related with floors and ceilings. Eg, in a single contract, it might be composed of: 60% fixed and 40% market-related or some other combination of percentages. This is entirely up to the two parties negotiating the contract.

While we recognize the bespoke nature of market-related contracts (not uniform across contracts and utilities), we do feel that price reporters could offer a new type of contract indicator, using blended floors/ceilings and/or averaging the floors/ceilings to show some forward level price. Again, we realize that this is not the most straight-forward endeavor as there are many pieces to these contracts, however when Cameco is publicly stating they continue to seek ~$70/lb floors and ~$130/lb ceilings, an average price of the floors/ceilings is $100/lb or 25% above base-escalated reported prices today. While no one knows what the spot price will be at time of delivery, the point is that everyone in the market can benefit from this information, utilities, suppliers, and investors.

Cameco Contracting Talking Points

We urge readers to listen to industry conference calls as you will learn more about how they are thinking about the market and their current strategy.

During Cameco’s Q1 2025 conference call, they discussed some of their views around contracting today.

Source: Cameco Q1 2025 Earnings Call, May 1, 2025

As we just noted above, Cameco’s CFO, Grant Isaac, is giving stakeholders and market participants immense insight into what they are seeing in their negotiations and what their current strategy is. Every investor needs to make it a point to listen to these conference calls.

Grant talks about several items that are very important to Cameco today:

Where are we in the cycle? Cameco wants market-related contracts which means they are bullish on the future price of uranium and want to capture that by receiving spot prices (or close to it) at time of delivery.

Cameco does not believe that the spot price weakness in the second-half of 2024 into early 2025 means they would need to lower their floor level offers as these contract deliveries will happen years into the future. As a result, they have no interest in lowering their floor offers of ~$70/lb to reflect for some nearby turbulence in the spot market.

Since different customers have different needs, Cameco can work with their customers offering a variety of floors and ceilings so both parties are content. Eg, if a utility believes the market can weaken in the years ahead (but Cameco does not), they could offer a more attractive floor to a customer while raising ceiling prices. The takeaway here is that market-related contracts with floors and ceilings can give counterparties a variety of options to find a suitable outcome.

Cameco continues to look for market-related contracts with floors that are $70/lb escalated and ceilings of around $130/lb. As he noted early, Cameco orients their contracts around where they believe the structural demand and supply is on a forward basis.

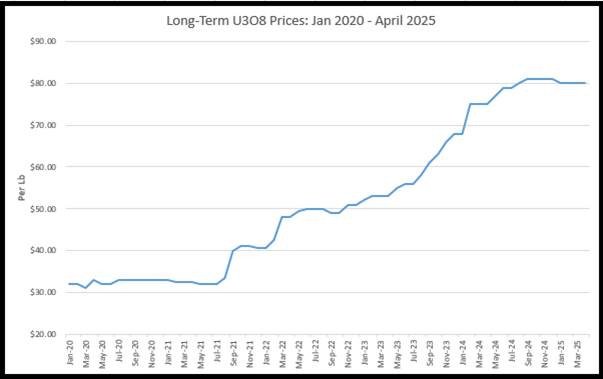

State of the Contract Market Today

Today, long-term uranium contract prices (base-escalated) sit ~$80/lb.

Source: Cameco Corporation

We know that Lotus Resources continues to sign pounds in and around these levels as they look to re-start their Kayelekera uranium mine in Malawi.

Source: Lotus Resources, Quarterly Activities & Cashflow Reports, April 30, 2025

As we can see from their MD&A, Lotus disclosed their latest contract as a base-escalated one, minus a small discount and escalated using the Royal Bank of Australia’s (RBA) long-term inflation escalator. As a result, we know the contract was signed ~$80/lb and will escalate each year moving forward until the contract’s completion.

Meanwhile, we know suppliers and utilities continue to hash out conversations. There are two ways utilities can approach contracting: sending a Request for Proposal (RFP) to the market for suppliers to respond to by a certain date or “off-market” discussions. RFPs are public in the sense that a utility will send a request to preferred (or all) suppliers in the market. As a result, the market will be aware of it as numerous entities have the option to respond to it with a price quote. Typically, suppliers will have a certain amount of time to decide and a utility will have a certain amount of time to award a potential winner of the contract.

Off-market or bilateral talks are when a utility approaches a supplier directly for a one-on-one discussion. Typically, a utility will have a strong history of doing business with the supplier and as a result, know each other well in terms of their typical needs, contract terms, etc. Generally, the market will not know about these discussions until they are disclosed. As we noted earlier, all contracts might not be disclosed to price reporters. However, price reporters do their best to understand all contracts in the market and where they are signed.

Final Thoughts

The purpose of this Deep Dive is to be a bit of primer on prices and the basics of them. However, we wanted to share a couple of final thoughts around prices.

Source: EIA 2023 Uranium Marketing Annual Report, pg. 27

The chart above, which comes from the EIA’s Uranium Marketing Annual Report (UMAR) breaks down the reported price that US utilities paid for a quantity-weighted average price for each of eight distributions. Basically, it gives us a view into the range of prices that US utilities had for price deliveries in 2021, 2022 and 2023. As a side note, the 2024 EIA UMAR should be released in the next couple weeks.

For 2023, we see is an enormous range of prices: from the first distribution of $23.24/lb all the way up to $72.97/lb. The takeaway for readers is that due to the variety of contracting types (and the ability to use the spot market opportunistically), we see utilities can pay a wide range of prices for any annual delivery depending on when they contracted, how they contracted and with whom they contracted.

So, while the base-escalated lowest offer is ~$80/lb today, utilities (suppliers and investors) need to consider how their contract books might be positioned and what the exposures are as multiple contracts and types are layered in over the years. As a result, it is important to understand that the latest spot and/or contract price is simply a snapshot at the moment of where buyers and sellers might interact. For investors, it means being conscious of these dynamics and being thoughtful about why utilities might very active or very quiet in the spot and/or term market.

From an equity investor perspective researching a producer or developer, it is very important to understand how a company markets their uranium and what they are trying to accomplish. For example, we discussed two companies in this piece, Cameco and Lotus Resources. Each company has vastly different characteristics due to their history in the market, their asset base, the jurisdiction, their cost structure (at the mine and corporate level), among many other items. As a result, we see a mature Cameco business looking for market-related exposures today as they believe prices will rise in the future while Lotus is just building out their contract book using base-escalated prices to have a thorough understanding of their revenue and cash flows as they look to re-start their Kayelekera mine in the back-half of 2025.

The uranium market is extremely dynamic due to these variables. As a result, it is up to every investor to understand the basics of prices, types of contracts available, how prices are reported and how these dynamics can affect a company’s revenue and cash flows.

We hope this serves as a basic 101 primer on how prices are formed and reported along with the types of contracts that exist and can be utilized by industry participants.

Thank you. Great piece. You have explained these pricing dynamics, which are difficult to learn from scratch, very well. (Context: I have been long the sector for a couple of years now.)

What kind of amount of reported long term contracts by uxc would you consider as replacement rate contracting, as a percent of total annual demand look like roughly? Besides a small amount procured from spot market by utilities, how many contrats will go unreported? Then, we have a very significant amount of production that is sovereign owned and supply their own and export reactors. Would Rosatom report (or even make a contract) for their production from Russia and joint ventures in Kazakhstan for their own reactors? How about CGN/CNNC for their owned production and Orano for the part of production they supply to EDF?