Over the past several quarters, some market participants have taken the view that lower uranium term contracting volumes are the direct result of not enough Western conversion capacity. The argument is, after Russia invaded Ukraine, some Western utilities began self-sanctioning against Russia by no longer entering new conversion (and enrichment) contracts with them. As a result, there is not enough conversion capacity in the West and utilities have been forced to stop contracting for uranium until more conversion capacity can come online.

The purpose of this Deep Dive is to examine the conversion market by reviewing the recent past that led to today along with our future views through 2030. We will examine:

· Who Are the Converters?

· Conversion: The Basics

· The Recent Past

· State of the Conversion Market Today

· Secondary Conversion Supplies

· Western Conversion Supply/Demand Model

Most importantly, we will draw conclusions about the narrative around western conversion capacities and any impact on uranium term contracting.

Below is a very simple diagram for the fuel cycle, starting with uranium mining. We assume many of our readers understand the basics of the fuel cycle so we will not delve into the details, but rather this is just a reminder of how uranium ultimately gets turned into fuel rods. There are many places to learn more about the details of the fuel cycle if one wishes to do so. But, today, we will be focused on the second step of the fuel cycle, conversion, where uranium is turn into a gas called uranium hexafluoride or UF6.

Who Are the Converters?

There are five companies that are involved in converting uranium (U3O8) to uranium hexafluoride (UF6):

· Cameco: Port Hope, Ontario, Canada

· Converdyn: Metropolis, Illinois, USA

· Orano: Tricastin, France

· Rosatom: Seversk, Russia

· CNNC: Diwopu & Hengyang, China

The western converters are comprised of three companies: Cameco Corporation, Converdyn (owned by Honeywell), and Orano (the French state-owned nuclear conglomerate). This leaves the eastern converters: TVEL/TENEX which are owned by Russia’s state-owned nuclear company, Rosatom and the state-owned Chinese nuclear company, China National Nuclear Corporation (CNNC).

Currently, Westinghouse owns the Springfields Fuel Ltd. (SFL) in the United Kingdom which is now owned 51% by Brookfield Renewable Partners and 49% by Cameco. However, the site currently sits idle and has not operated since Cameco ended a toll-conversion agreement with them in August 2014 as the bear market began to accelerate after the Fukushima disaster in March 2011.

Conversion: The Basics

Uranium leaves the mine as a stable oxide concentrate otherwise known as U3O8. There are two conversion processes used by conversion plants or converters. The main process, known as “wet” which is used by Cameco, Orano, CNNC and TVEL/TENEX.

This process begins by dissolving the concentrate into nitric acid. The resulting clean solution of uranyl nitrate is fed into a countercurrent solvent extraction process, using tributyl phosphate dissolved in kerosene or dodecane. The uranium is collected by the organic extractant and can then be washed out by diluted nitric acid solution and then concentrated by evaporation. The remaining solution is the calcined in a fluidized bed reactor to produce UO3 (or UO2 if heated to the proper level). This reduced oxide is then reacted in another kiln with gaseous hydrogen fluoride to form uranium tetrafluoride (UF4).

The UF4 is then fed into a fluidized bed reactor with gaseous fluorine to produce uranium hexafluoride (UF6) which is condensed and stored for shipment.

The alternative process, known as “dry” is used by Converdyn in the United States. In this process, the concentrate is calcined to remove some impurities then crushed. At Converdyn, the U3O8 is produced into an impure UF6 then refined via a two-stage distillation process.

UF6 can be highly corrosive, especially if moist. When it is warmed to a gas, it is much more suitable for the enrichment process in centrifuges. At lower temperatures and under the proper levels of pressure, UF6 can be liquified and it filled into specially designed steel shipping cylinders which weigh over 15 tons. As the material cools, the liquid UF6 turns into a white crystalline solid and is shipped.

Source: World Nuclear News (WNN)

The Recent Past

It is very important to understand what has happened in this little corner of the fuel cycle over the past 20 years as persistently low prices has helped shape the market into what it is today. Simply put, for many years, the conversion market was stable, but low prices and abundant inventories meant that conversion made up just ~5% of the total fuel cost for utilities. As a result, while conversion is an essential step to producing nuclear fuel, it became somewhat overlooked.

Source: UxC, LLC

Post-Fukushima, the first supply curtailments started at Springfields Fuel Ltd. (SFL) conversion plant in the United Kingdom in 2014. In 2005, Cameco had signed a 10-year toll-conversion agreement with Springfields to process up to 5 million kilograms (KgUs) of uranium. SFL would receive the uranium trioxide (UO3) from Cameco’s Blind River uranium refinery and covert it to UF6 and Cameco would then deliver it to customers around the world.

While the toll-conversion agreement was set to expire in 2016, Cameco agreed to pay $18M to SFL as an early termination fee. As a result, production at SFL ceased on August 31, 2014. At the time, with conversion spot prices hovering ~$7.50/KgU, Cameco’s CEO Tim Gitzel remarked, “With the current weak market for UF6 conversion we can meet our customer requirements from our Port Hope conversion facility and benefit from better utilization of existing assets.”

Several months later, in July 2014, Converdyn announced that it had been denied a temporary injunction for the US Department of Energy (DoE) to stop the government’s UF6 barter program. Under it, the DoE was authorized to sell a predetermined portion of UF6 inventory to pay Flour-B&W Portsmouth, the DoE’s contractor for the decontamination and decommissioning of the Portsmouth Gaseous Diffusion plant in Piketon, Ohio.

Converdyn argued that, under Federal law, the DoE is prohibited from making transfers unless the Secretary of Energy determines those transfers will not have an adverse impact on the US nuclear industry saying, Converdyn “has repeatedly provided information to DoE demonstrating that the transfers would and do have a substantial adverse impact on the domestic conversion industry, in part because the government will receive less than fair market value.” Effectively, the US government was using UF6 stocks and dumping it into the market (through an intermediary) to help pay for the cleanup of the Piketon plant.

As it turns out, Converdyn was not lying about the market impact to their business. In November 2017, Converdyn announced that they were shuttering the United States only conversion plant as priced approached cycle lows of ~$4.50/KgU. They company said its decision to suspend production was the result of “significant challenges” faced by the nuclear industry, including a situation with a current worldwide oversupply of UF6 and noted the decrease in demand from Japan and Germany following the Fukushima accident.

Converdyn was quite savvy about the situation. The plant had closed for routine maintenance in October 2017 and it is now clear that internally, the company had decided to shutter the plant beyond just routine maintenance. They knew that production costs were well above spot market prices, so Converdyn began buying conversion (by purchasing UF6) in the open market. Prices bottomed in November 2017 at the time of the closure announcement and by April 2018, they had already perked back up to $8/KgU. By summer, prices were closing in on $10/KgU and by year-end 2018, spot conversion was changing hands at nearly $14/KgU.

Source: UxC, LLC

Converdyn shutting down its Metropolis in November 2017 marked the bottom for conversion prices. Since Converdyn had accumulated conversion in the open market at depressed prices, the converter was able to continue to make deliveries without any primary production. It was not until April 2021 that they announced the re-opening of CVD by 2023, costing ~$150M to do so.

The market was helped along with the DoE ending its UF6 barter program that helped pay for the cleanup at the Piketon, Ohio gaseous diffusion plant.

State of the Conversion Market Today

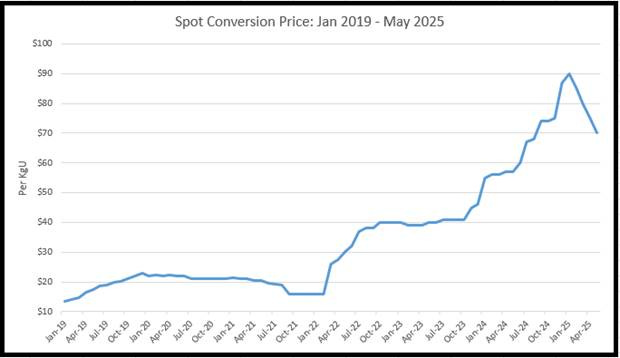

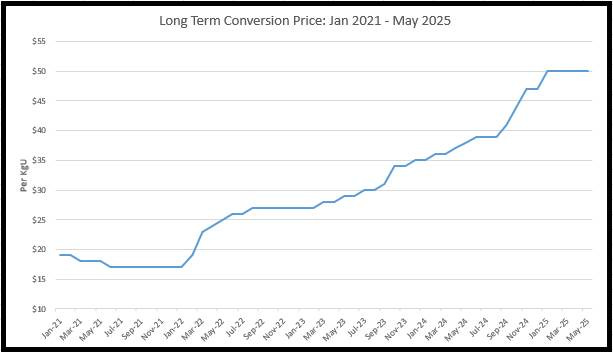

This set up brings us to today, where conversion prices are at a place they have never been in the history of this industry. Spot prices trade hands ~$70/KgU with long-term contract prices resting at $50/KgU.

Source: UxC, LLC

It should be no surprise that conversion prices moved up significantly after Russia invaded Ukraine in February 2022. Russia had ~25% of global capacity at the time and even more of actual production percentage since Converdyn was still not running since being put into care and maintenance in November 2017.

Today, while spot prices sit ~$70/KgU off their record of ~$90-$100/KgU, long-term contracts remain at $50/KgU, at all-time high prices which continue to reflect supply tightness.

Source: UxC, LLC

The conversion remains the weakest link in the fuel cycle and lacks significant investment, particularly in the West. It is unrealistic to think that any meaningful new primary conversion supply can come online within the next several years. As a result, any short falls through the end of the decade will need to be covered using existing primary supply and secondary supplies.

Converdyn

Converdyn (CVD) re-started their Metropolis plant in mid-2023 after almost six years offline. Our understanding is the plant targeted ~7M-KgU in 2024. With the plant returning to its normal run rate and if de-bottlenecking efforts can be introduced, it appears the plant could run slightly higher than just 7M-KgU, although we will need to wait and see if production moves up.

While it is possible to expand Metropolis, there are no expansion plans now. The company has been quite clear that to expand, their sales book would need to be underpinned by higher sales prices and longer duration contracts to underwrite the capital expenditures. Based on recent commentary from the company, utilities have shown little interest to “pay up” beyond what is being offered in the market. While somewhat anecdotal, this tells us that while primary conversion capacities are tight, they are not dire enough to cause utilities to help underwrite any expansion. As a result, this is a piece of information that lack of conversion is not causing lower levels of uranium term contracting.

With that said, it is important to recognize that the conversion business has not been wildly profitable for decades. Can we blame CVD for not wanting to spend large capital expenditures to expand capacity when the business itself has faced headwinds for decades?

Additionally, we do not expect any plans to add new capacity as Honeywell is currently being targeted by activist investors to split up or spin out assets. In this environment, we find it hard to believe that any expansion is imminent.

Cameco

Cameco’s conversion business is composed of two sites: their Blind River refinery and Port Hope Conversion Facility (CMC). Blind River takes uranium concentrate, purifies it, and produces UO3. It is then transported to the Port Hope facility to be converted into UF6.

Port Hope continues to operate well, producing 10.8M-KgUs of UF6 in 2024 with 2025 guidance targeting 13-14M KgUs of total production (UF6, UO2 and heavy water reactor fuel), all of which has already been sold into existing contracts. As a result, we believe 2025 UF6 production will be between 11M-11.5M-KgUs. In Q1 2025, they produced 3.9M-KgUs (all products), which was a 5% increase over Q1 2024.

Cameco has been working to expand Port Hope but noted that inflation, availability of qualified labor, aging infrastructure/equipment, and the impact of supply chain challenges on the availability of materials and reagents have meant that any increases in production have been relatively slow.

It is also known, via their filings, that they have been supplementing its conversion production with loans and purchases from others in the market. As of Q1 2025, Cameco had loaned Orano ~1.15M-KgU of conversion supplies in 2022 and 2023 with those quantities needing to be returned by December 31, 2035. Cameco can borrow up to 2M-KgU of UF6 by September 30, 2027 without repayment in kind up to December 31, 2027. As of March 31, 2025, Cameco has borrowed 1.49M-KgUs of which, 293K-KgUs and 1.197M-KgUs would be repaid in 2025 and 2026 respectively.

We believe Port Hope’s UF6 production should remain relatively steady as it pushes closer toward 12M-KgUs of supply per year in the next couple years.

While Cameco keeps its available capacities close to the vest, we know that they only sell into the term market. With prices at $50/KgU, we assume new contracts for any customers will be at or above this level.

Orano

Orano’s conversion business is composed of two sites: the Malvesi plant and COMURHEX (CMX). The Malvesi plant, which handles the first phase of uranium conversion, purifies the natural uranium concentrate and produces uranium tetrafluoride (UF4). The second facility, Orano’s COMURHEX (CMX) plant completes the conversion to uranium hexafluoride (UF6). CMX continues to ramp up operations of its CMXII facilities in southern France focusing on the new Philippe Coste UF6 plant.

Orano has targeted higher production levels in the face of operational challenges, including labor disruptions late in 2024. While infrastructure issues have been reduced, the output in since 2023 has remained roughly the same, ~10.5M-KgUs and expect production to move up to ~11M-11.5M-KgUs in 2025.

Orano is aiming to increase UF6 production by roughly 1M-KgUs per year over the next couple of years, targeting 13.5M-KgUs by 2028. While there are still some challenges, we remain optimistic that operations will improve. Typically, we see improving performance as equipment and other technical issues are overcome and run rates persist for longer periods. Orano continues to fulfill contracts from primary production, inventories, loans (from Cameco) and open market purchases.

Rosatom (TVEL/TENEX)

Rosatom runs its sole conversion plant in Seversk, Russia which is owned and operated by TVEL with TENEX managing other aspects of the business like marketing the material. While Russia offers little UF6 directly, its conversion capacity and output play a key role in ultimately creating the types of material they sell.

Obviously, Russia’s business has been affected since it invaded Ukraine in February 2022. The key item is that multiple countries from the West have effectively self-sanctioned and have not signed any new contracts with them. It is important to note that some Western customers continue to take deliveries of legacy Russian contracts. Currently, the United States has a ban of Russian material with waiver exceptions. While some deliveries have been made to the United States via the waiver process, questions remain on how many more will come, even if a US utility has a waiver. The amended Russian Suspension Agreement (RSA) calls for a complete ban of Russian material (with no waiver process) by January 1, 2028.

It is well-known that Western demand for Russia’s conversion services will continue to drop moving forward, even if the war in Eastern Europe is resolved soon. We have seen plenty of evidence of this as VVER-reactors in Eastern Europe turn away from Rosatom and embrace Western suppliers.

The flipside to these Western market losses is that Russia maintains a robust domestic and export reactor program and will continue to service these new builds with a vertically integrated fuel cycle, including conversion.

One aspect that is less discussed in the market is the return feed in the form of U3O8 or UF6. Let us run through a couple basic examples. If a utility signed a contract for conversion + SWU, Russia will ship EUP and the utility will return U3O8 to Russia, thereby isolating what the contract was for, in this case, conversion + SWU.

If a utility signed a SWU contract, Russia would ship EUP and the utility would return UF6 (uranium + conversion) back to Russia.

The point is, depending on the type of contract, return of some material typically takes place.

With the war, western countries sanctioned numerous Russian entities. As a result, some western entities began to refuse shipping back any return feed for fear of also being sanctioned by their own government or another western government. This has created challenges for Rosatom who have found themselves short feedstock material (U3O8 and/or UF6). Also, since cylinders were not being returned to Russia, there are rumors that they also face a shortage of cylinders to move material around.

Today, we believe the total capacity at their Seversk plant is 12.5M-KgUs and understand that they have been implementing some production capacity modernizations since 2023. As a result, we expect capacity to increase over the next several years reaching 15M-16M-KgUs by the end of the decade. These additions will be used to fuel their domestic and export needs along with China’s vociferous needs.

China National Nuclear Corporation (CNNC)

CNNC manages all of China’s domestic fuel cycle capabilities via a subsidiary, China Nuclear Energy Industry Corporation (CNEIC) including the marketing of conversion, enrichment, and fuel fabrication.

China’s continued reactor program growth means it continues to invest in its fuel cycle capacities.

The country runs two conversion plants: Plant 404 in Diwopu and Plant 272 in Hengyang. Plant 404 has two facilities, the original on-site plant capable of 3M-KgUs and newer plant that came online in 2018 for another 6M-KgUs brining Plant 404 total capacity to 9M-KgUs. Plant 272 also came online around the same time of the second facility at Plant 404, which has a capacity of ~3M-KgUs. Our understanding is that Plant 272 continues to increase production inline with enrichment feed requirements.

Springfields Fuels Ltd. (SFL)

As mentioned earlier, SFL is owned by Westinghouse (WEC), which in turn, is 51%-owned by Brookfield Renewable Partners and 49%-owned by Cameco. There is no doubt that the Western markets are looking for new sources of UF6 supply. In 2022, the UK government awarded WEC a £13M grant to conduct studies on re-starting the plant from the UK Department of Business, Energy, and Industrial Services (BEIS). The award, alongside ongoing investments from WEC, will be used to prepare the necessary design and enabling work to begin new conversion capabilities. At the time of this announcement, a potential re-start date of 2028 was listed however we now know that this timeline is unrealistic.

In 2023, the UK government released £75M in funding to support the development of alternatives to Russian fuel supply as this funding to WEC will help the company develop primary conversion as well as capability for both reprocessed uranium and freshly mined natural uranium.

Company representatives have noted that the facility plans to have ~5M-KgUs of capacity with the goal of making a final investment decision (FID) sometime in late 2025 or early 2026. It is important to realize that conversion plants are effectively eating themselves alive with acid once you begin production. SFL has not run since 2014 and we suspect that the plant will need significant upgrades or total replacement of equipment. Further complicating any restart plan, who will provide the capital? The UK government has already expressed interest in seeing it re-started and has backed their view with some capital. Will WEC be totally responsible for the re-start? Will the UK government help fund it? Or is WEC relying on utilities to underwrite the needed capital expenditures?

It isn’t totally clear to us how this situation will resolve itself and when. We believe that a key portion of any FID will ultimately be market related, eg, utilities will need to sign properly priced and duration term contracts that help underwrite the capital expenditures required to get the plant online. But, as we noted in the CVD section, the conversion business has been difficult for suppliers going on 35 years now. It is not clear that primary suppliers, including WEC will simply start pouring capital into a facility unless the demand signals are extremely robust and/or if the government is willing to foot some of the bill.

Secondary Conversion Supplies

Like the uranium market which has secondary supplies, conversion is similar. These supplies can, generally, come from the following:

· Government Inventories: These primarily come from material held from nuclear weapons programs in the past. The US and Russian governments are largest holders of these inventories and must be processed to fit any civilian usage. Supplies from governments have dropped sharply over the years, like when the US government suspended the UF6 inventory barter program. The main source of US government supplies comes from Highly Enriched Uranium (HEU) down blending used by Tennessee Valley Authority’s (TVA) tritium-producing reactors. We model this supply at 0.6M-KgUs for 2025 and steady state per year moving forward.

· Enricher Sales: Underfeeding and/or re-enriching tails had resulted in large quantities of UF6 entering the market but their role in these activities has severely diminished in the past couple of years. Western enrichers have rapidly reduced underfeeding, especially since the Russian invasion of Ukraine. We believe this will be effectively phased out shortly. We model 1.0M-KgUs of UF6 for 2025 and 2026 from western sources (mainly Orano) and then phase them out to zero by 2027. If we are wrong and some material does hit the market from an enricher, this helps balance the conversion market for western utilities.

· Utility Inventories: Utilities always hold inventories in various forms including UF6. We have a pretty good idea how much US and European utilities hold in inventory (along with which form) from the US’s Energy Information Administration’s (EIA) Uranium Marketing Annual Report (UMAR) and Europe’s Euratom Supply Agency (ESA). The latest EIA report from May 2023 shows US utilities holding 30.9M-lbs of natural UF6 (in U3O8 equivalent pounds). In Europe, the ESA’s 2023 report showed utilities holding a combined 21M-lbs of natural UF6 (in U3O8 equivalent pounds). We model US + EU utilities using 4M-KgUs (~10.4M-lbs of U3O8e) of UF6 inventory to fulfill their needs in 2025 and slips to 3M-KgUs for the remainder of the decade. Please note that we do not count any enriched UF6 as a part of these inventories.

· Other Commercial Inventories: This category can include uranium trading houses, banks, hedge funds and/or physical sequester vehicles. At present, both Sprott Physical Uranium Trust (SPUT) and Yellow Cake PLC hold no UF6. It is unknown the precise amount that the others could hold. We know from the EIA UMAR that some traders can hold this material and have held speculative longs in the recent past (especially from when spot conversion prices went from $50/KgU to nearly $100/KgU). We model this to be 2M-KgUs per year through 2030.

· MOX + RepU: A select few countries are involved in reprocessing spent fuel and recycling any reusable material, including reprocessed uranium (RepU) and mixed-oxide uranium/plutonium (MOX) fuel. Japan and France (along with Russia) are the main users of recycled products. For the purposes of this piece, the important item to note is that MOX replaces the need for conversion. We model a steady state 2.0M-KgUs of RepU + MOX for Japan and France through 2030.

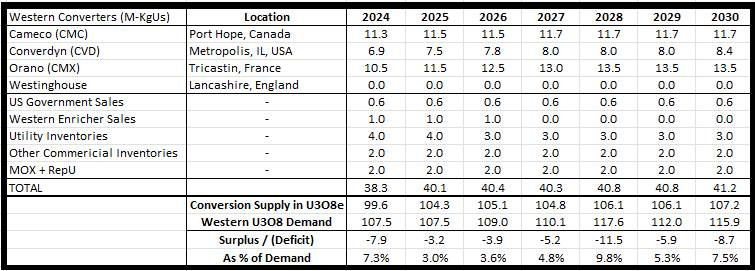

Western Conversion Supply/Demand Model

Below, we have laid out the various inputs:

· Western Primary Conversion Supply in M-KgUs

· Secondary Conversion in M-KgUs

· Total Western Reactor Consumption (Demand) which include: Belgium, Canada, Czech Republic, Finland, France, Netherlands, Romania, Slovenia, South Korea (65% of needs), Spain, Sweden, Switzerland, Ukraine, United States, and the United Kingdom

· To calculate M-KgUs to U3O8e (equivalent), multiply by 2.6

As you can see from our model, when we line up total western conversion supply (primary and secondary) against western demand, the market is in deficit. The argument that some have been making, is that, this deficit is big enough to slow down or stop utility term uranium contracting.

Well, beyond the basic notion that utilities have a nuclear reactor to run and will continue to procure like they always do, why would a deficit stop a market from functioning? Said differently, when has a market ceased to function or end-users simply stop their procurement due to tight supply capacities? We feel that this view is unrealistic for several reasons.

First, price is the ultimate determinant in a market. We have talked about the explosive move in the conversion market over the past several years, especially since the Russian invasion of Ukraine. The high price is solving for the shortages as it brings out inventory. Whether that inventory is from a utility, trader, bank, hedge fund or government (not relevant here beyond TVA’s contract), the market will solve for it.

Secondly, this model does not consider any conversion or conversion-held components that western utilities are still receiving from Russia. Some countries, including the US, continue to receive legacy contract deliveries from Rosatom. While the exact quantities are not known, we do know some deliveries continue to happen, making any deficit we show a bit too large, at least for 2024 and 2025. We urge all market participants to continue to watch for waivers and shipments to the US from Russia.

We also know that a trading group, at least previously in the 2023-2024 period, had been purchasing Chinese EUP and selling it all or components to US utilities. While we do not think this was being done in enormous volumes, the trader capitalizing on high prices (eg, the market solving for shortages). We do not expect much more material to come from this source since tariffs have gone up in 2025 (from 10%) during the Trump Tariff…Tantrum…War?

For the 2025-2030 period, the total deficit in U3O8e is 38.4M-lbs or 6.4M-lbs per year. Is this enough to stop utilities from contracting? This seems very unlikely to us as we believe utilities have used the last few years to ensure coverage of the most important windows to them, in this case, through the end of the decade. While there is a narrative among some investors that utilities are naïve, we disagree with this notion and believe they have been hyper-sensitive to the dynamics in conversion to ensure they have proper coverage.

While Cameco and Orano are slowly trying to increase production, we have not seen Converdyn expanding capacity. If the supply situation were so dire that it had an impact on uranium contracting, we believe we would have already seen new capacity announcements underwritten by even higher term prices than they are today. However, we want to temper this view with something we wrote about earlier.

And that is, we believe conversion capacity expansions can only happen in an environment where western converters are certain they will see a return on their investment. While it appears the market is bifurcating without Russia, will the market look like this in five years? How about ten or fifteen? Due to this uncertainty, we do not believe western converters are in any material hurry to add capacity.

Further, given that some western governments, especially the US government are dangling billions of dollars to help rebuild the US fuel cycle, will a company decide to start investing their own capital first? Or, wait to see if the government can help fund expansion projects? The main point is the market always seems put the ball in utilities court, but there are relevant reasons why a supplier might not want to rush ahead.

Lastly, we know term conversion contracting volumes have been very robust since the Russian invasion. Anyone who has been around this market knows that western utilities have been most focused on conversion and enrichment since Russia is such a large piece of those markets. We believe that European utilities, who tended to do more conversion business with the Russians than the Americans, really needed to make a shift at the end of Q1 2022 which is a big reason why conversion prices began to rise so rapidly after the war began.

Said differently, utilities have been doing their job by securing their downstream services (conversion and enrichment) so they can feed the product (natural uranium) into those service contracts to get what they ultimately need, enriched uranium product (EUP).

From 2022-2024, global term conversion contract volumes totaled nearly 117M-KgUs, or ~304M-lbs U3O8e. Over a three-year consecutive period, we believe this is the most conversion ever booked in the history of this market. We recognize that these contract volumes are for global utilities, not just western ones. However, we think it is rather obvious that it is the western buyers (especially Europeans) have been most active in term conversion contracting. Other countries, who continue to do business with the Russians will have the ability to contract for conversion with a lot less difficulty given their supply capacity.

When we add up the hard data and context of the market, we firmly believe that these western conversion deficits are simply not large enough for an industry to simply shut down buying of the needed feedstock, U3O8.

The speculative fervor that reached a fever pitch in the spot market this past December/January has also subsided, with spot conversion prices backing up to ~$70/KgU from the $90-$100/KgU levels. Current offers are still very elevated on a historical basis but the market is showing signs of cooling which leads us to believe, any nearby uncovered needs have been fulfilled.

Long-term prices continue to trade at $50/KgU as the market continues to solve for the capacity tightness.

We believe we have laid out a reasonable case as to why western supply tightness is not the key reason for reduced uranium contracting volumes. Do we believe they need to turn their attention to uranium in a more meaningful way soon? Yes, we do. And we believe that contracting will pick up as we progress through 2025 and into 2026.

We are hopeful that this gives readers a better understanding of the recent history in conversion, the converters, their capabilities and whether capacity tightness in conversion has led to a lack of uranium contracting. Given what we laid out with the primary and secondary supplies vs. reactor consumption, we feel this narrative can be put to rest.

Thanks for an excellent piece.

Once EUP is enriched to the required assay, the UF6 needs to be converted back to U metal or U oxide. Why isn't this second conversion step shown in the ubiquitous fuel cycle chart like you're provided? Is it the same companies that do the reverse conversion? Does it complicate the picture you've painted?

Brilliant piece as always!

Another element that could be contributing to the hesitancy to invest in expanding conversion capacity is emerging enrichment technologies that bypass the need for conversion, like what ASP Isotopes and Ubaryon are working on.